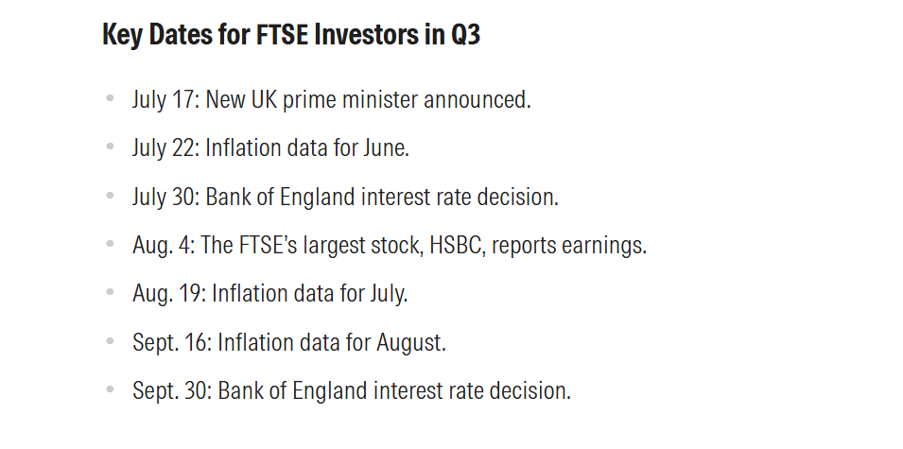

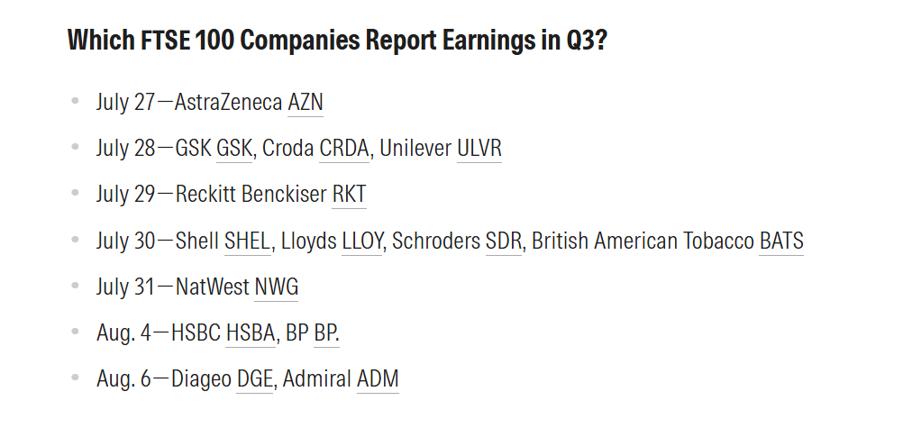

What’s the Q3 Outlook for the FTSE 100?

UK stock and bond investors face political uncertainty again as FTSE companies clarify the impact of the Iran war on their earnings.

Ollie Smith

Ollie Smith

The following article was published by  .

.

Key Takeaways

The FTSE 100 enters the third quarter with investors weighing a change in UK government, fresh inflation data, Bank of England interest rate decisions, and the upcoming earnings season. Globally, the AI boom, US interest rates, and geopolitical events will also be key drivers of the FTSE 100 and FTSE 250 as the indexes seek to regain the record highs touched at the start of the year. A strengthening US dollar is also a factor for UK investors for the rest of the year.

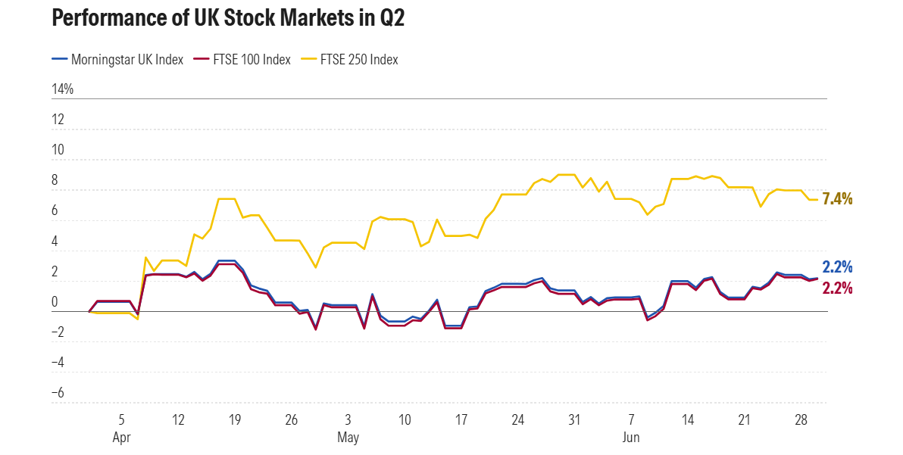

After a shaky start triggered by the Middle East war, UK stock markets enjoyed a more stable Q2, with the Morningstar UK Index rising around 2% between April 1 and June 30 in GBP terms, the same as the FTSE 100. The mid-cap focused FTSE 250 made stronger gains, rising 7.4% in the three months to the end of June. In the year to date, the FTSE 100 is around 7% higher and the 250 nearly 5% higher.

Source: Morningstar. Data as of June 30, 2026.

What Will FTSE Companies Say About Inflation and the Iran war?

Stock markets may have reacted positively to a period of relative calm on the international front, but investors will likely hear some significant updates about the effect of the conflict between US and Iran on company earnings guidance in Q3.

In the UK, the inflationary impact of the conflict has not been quite as bad as originally feared, but significant uncertainty still surrounds how policymakers will react.

“Central banks worldwide may still have to increase rates, as the European Central Bank did on June 17, but the belief in markets currently is that any upward move will be short-lived, before we return to a lower interest rate environment,” say Morningstar’s Michael Field and Fabienne Pfeiffer, chief European market strategist and associate equity analyst, in a note.

For now, UK rate cuts are “off the table” in July, according to the Bank of England’s governor Andrew Bailey. That doesn’t mean there won’t be rate cuts later to stimulate the UK’s economy. Still, futures markets currently show no interest rate increases for the rest of 2026.

“Higher inflation and rising interest rates, paired with already meek economic growth, could begin to strain households and corporations,” Field and Pfeiffer add.

How Will UK Bond Markets React to an Andy Burnham Government?

A now-certain change of government and potential bond market turbulence will be among UK’s big market narratives in Q3 as the country gears up for its seventh prime minister in just over a decade.

“Persistent political fragility is a clear symptom of the deeper structural, fiscal, and social challenges facing a medium-sized economy adapting to rapid global shifts,” says Michael Diamontopoulos, associate director for fixed income and currency at Morningstar. It underscores the “long-term, compounding friction” that Brexit continues to exert on the UK’s long-term growth capacity, he adds.

When Keir Starmer announced his resignation in late June, UK gilt yields stayed steady.

“His decision to form an economic advisory team comprised of heavyweights like former BoE chief economist Andy Haldane and former Office for Budget Responsibility chair Richard Hughes sent a well-received signal to the bond market that the incoming leadership is acutely aware of market scrutiny and recognizes that the margin for fiscal error is practically non-existent,” says Morningstar’s Diamontopoulos.

There could still be turbulence ahead, however. Andy Burnham has already committed to some big-ticket spending, including the state pension triple lock, and defense analysts also suggest the recently revised Defence Investment Plan will leave his new chancellor with unfunded costings. This could impact both gilt markets and the UK’s stable AA credit rating. A smooth transition of power to Keir Starmer’s successor is essential, experts suggest.

“Any credit implications of the leadership change will depend more on the quality and durability of the incoming government’s policy agenda, the new cabinet composition, and the degree of commitment to the existing fiscal policy trajectory,” a note from Morningstar DBRS says.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

Please Note:

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy.

The above article was first published by Morningstar and should not be regarded as individual investment advice on whether to buy, sell or hold any of the investments mentioned. Please speak to Ethical Offshore Investors or your personal adviser BEFORE you make any investment decision based on the information contained within this article.

At Ethical Offshore Investments, our clients can access a range of investment option to gain exposure to the UK equity market. This can be in the form of low cost index ETF’s / funds or active specialist Fund Managers. Either way, we do not charge any additional upfront fees. To learn how you can save on your investment costs, speak with us now – lower costs result in more of the investment growth staying in your pocket

Socially Responsible Investing – Ethical Business Standards