Can emerging market equities outperform in the next decade?

Today, the environment could be far more favourable for this area of investment – peaking interest rates, a weaker dollar, falling energy prices, and a more normalised economy in China, could bode well for the asset class in 2023

Chris Salih – published by FundCalibre

The early part of the 21st century saw emerging markets outperform. Having survived a number of currency crisis in the late 1990s, the noughties were a time of stabilisation and growth for these areas.

In fact, while developed markets recovered from the tech bubble and then slid towards the sub-prime disaster that was the great financial crisis, emerging markets returned over 240%* in the first ten years of the new millennium. In contrast, the FTSE All-Share turned just over 25%* and the S&P 500 made a loss of 12%*

Then everything changed. A decade of easy monetary policy meant the US stock market was really the only show in town. Since the start of 2010 to date, the S&P 500 has returned just shy of 493%** compared with 149%** from the UK stock market and 92% for emerging markets**.

But now the investment environment has changed once again, is there reason to think emerging markets could excite investors once again? Could past performance be repeated?

How emerging markets have changed in the past decade

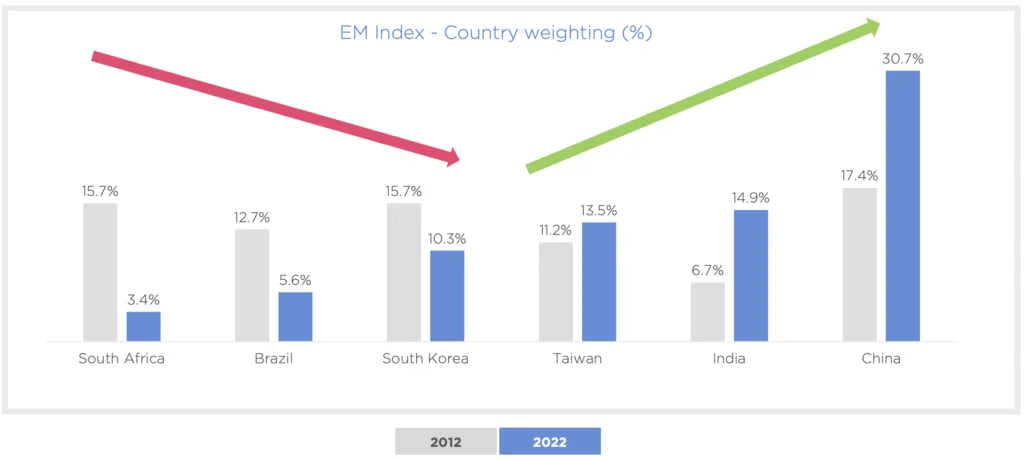

Over the past decade, the composition of emerging markets have changed significantly. Where South Africa once dominated, China has risen. Brazil and South Korea have fallen in prominence while Taiwan and India have grown***.

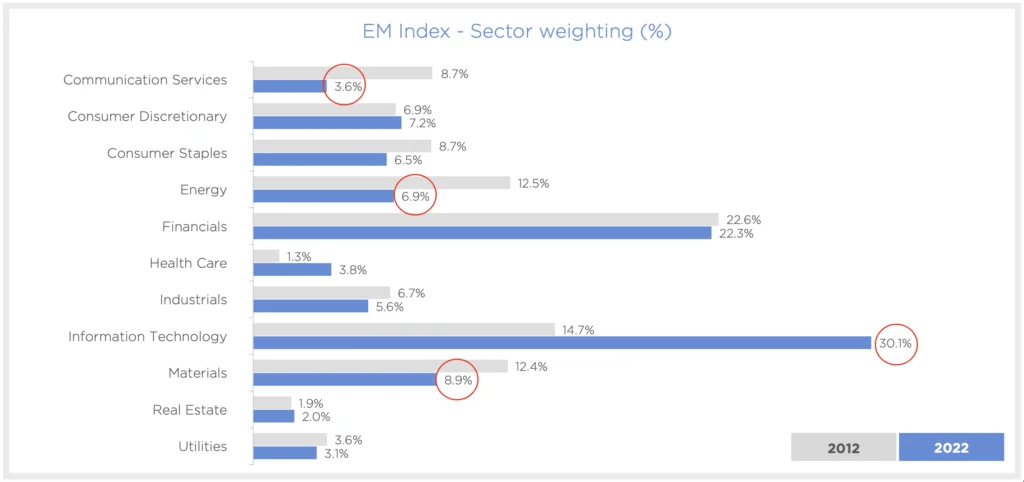

Sectors have also changed. Energy, materials and communication services sectors have all seen their market share decrease, while information technology in particular has flourished***.

And stock picking in this asset class has become key, as the number of companies in the MSCI Emerging Market index has ballooned by almost 50%. The index is now home to 1239 constituents***.

Graphic 1: Emerging Markets have changed in the last decade****

Graphic 2: Technology now dominates the EM index****

The attraction of emerging markets today

Developing economies have always been a growth story, and that has not changed.

They make up 45% of the global economy (vs 38% in 2012)*** and are experiencing population growth of 1% per annum compared with just 0.2% in developed markets***.

Today, the environment could be far more favourable for this area of investment – peaking interest rates, a weaker dollar, falling energy prices, and a more normalised economy in China, could bode well for the asset class in 2023. And, while it may take some time for these dynamics to play out, there could be good reason to be optimistic.

Fund managers around the world seem to be of this view. According to the latest Global Fund Manager survey by the Bank of America, their allocation to US equities collapsed in January, with respondents stating that their net underweight in the asset class stood at 39%, the lowest since October 2005 (52%). Instead, professional investors reallocated towards emerging market stocks, increasing their net overweight to 26% – the highest since June 2021.

What the fund managers are saying

Daniel Hurley, portfolio specialist at T. Rowe Price, believes there are several factors that should see a strong period of relative performance for emerging markets going forward.

“Valuations are highly compelling relative to developed markets, that, combined with China re-reopening, earnings momentum and the US dollar falling, could see a sustained period of outperformance,” he said.

“China re-opening is clearly the biggest catalyst after almost 3 years of pandemic restrictions; this will be very supportive for the consumer sector domestically also the asset class globally.

It will also be supportive for earnings momentum; emerging markets had the painful reset of earnings in 2022 and should inflect from a low base, this contrasts with markets where earnings have yet to reset and will be of key focus going forward.

“Finally, with the US economy weakening, the dollar could continue to depreciate from high levels. This is supportive for emerging markets; importers will benefit from the falling price of dollar priced imports and countries with dollar-denominated debt loads will also benefit from some respite.”

Tim Love, investment director, at GAM describes emerging market valuations as being, “like a coiled spring,” and says there could be a number of catalysts that spark material up-side for investors.

“15 years of choppy sideways performance is comparable to compressing a coiled spring,” he said. “A series of positive risk return opportunities are now in place (market downturn/Covid/oil shock), which rhyme with the situation in 2003-2008 (post Asian crises/SARS). Light liquidity, low positioning and negative sentiment could drive an attractive prospective risk/return for EM equities in 2023, in our view. Playing defence is yesterday’s game.”

Rob Brewis, co-manager of the Aubrey Global Emerging Markets Opportunities fund, adds that while there is inevitably some de-risking underway in global supply chains as manufacturers seek to diversify their production away from China, “this is all turning up in India (viz Apple’s vast new phone-making cluster outside Chennai), Vietnam, Mexico, and Indonesia to name a few.” In other words, it is very positive for most emerging markets.

“With one or two notable exceptions, the latter part of 2022 has been a period of weakening commodity prices. For most emerging market consumers, this is very good news,” continued Rob. “The changing energy landscape is also a long-term positive for most emerging markets. India is the standout winner in this, being short oil and long solar, at least in terms of potential. Russia, to which we have had no exposure in recent years, is the standout loser.

“Perhaps the final positive for emerging markets is US monetary policy. Whether US rates are near a peak is open to debate, but there are signs that the dollar strength might at least be abating, which makes it much more comfortable for emerging market central banks.”

“Whether it is the formalisation of the Indian economy, the continued financialisation of the South African population or the growing adoption of enterprise resource planning software in Brazil, there are plenty of growth opportunities to tap into,” concludes Rasmus Nemmoe, manager of FSSA Global Emerging Markets Focus.

Five emerging market equity funds to consider

Investors considering emerging markets could consider the following Elite Rated and Radar funds:

Aubrey Global Emerging Markets Opportunities invests in companies offering products and services to the upwardly mobile, ambitious, and aspirational population centres in emerging markets which account for over 70% of the world’s growth.

Federated Hermes Global Emerging Markets SMID Equity is a concentrated fund focusing on small and medium-sized companies across global emerging markets. It can also invest in frontier markets should opportunities arise.

FSSA Global Emerging Markets Focus fund invests in 40-45 large and medium-sized companies in emerging markets. Manager Rasmus Nemmoe has an absolute return mindset and looks for quality companies that can demonstrate sustained and predictable growth over the long-term.

GQG Partners Emerging Markets Equity is a concentrated portfolio of high quality companies with durable earnings. The emphasis is on future quality, rather than companies which have simply done well historically.

JPMorgan Emerging Markets Investment Trust has an established long-term track record of investing in emerging market equities. The extensive team at JPM take a long-term approach and focus exclusively on companies, rather than countries, in the emerging markets space.

*Source: FE fundinfo, total returns in sterling, 31 December 1999 to 31 December 2009

**Source: FE fundinfo, total returns in sterling, 31 December 2009 to 3 February 2023

***Source: Alquity, October 2022

****Source: Alquity, Bloomberg, October 2022

Photo by Joshua J. Cotten on Unsplash

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions. Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice. Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you.

Please note the above article was first published by Fund Calibre and should not be regarded as individual investment advice on whether to buy, sell or hold any of the funds mentioned. Please speak to Ethical Offshore Investors or your personal adviser BEFORE you make any investment decision based on the information contained within this article.

At Ethical Offshore Investments, we can access the funds mentioned in this article on the various offshore investment platforms we offer. We do NOT CHARGE any additional entry and/or exit fees to purchase these funds for our clients.

As we aim not to use commission paying funds, we will access the lowest charging version of the managed fund that is available on the relevant platform…… resulting in more of the investment growth staying in your pocket.

Speak with Ethical Offshore Investments to learn how you can save on your investments costs by investing via Ethical Offshore.

Socially Responsible Investing – Ethical Business Standards