SustainAbility – Goldilocks & the two Bears

One of the few things that we can be certain about is that the future is uncertain.

The events since early 2020, which have included a global pandemic, a war in Europe and a rise in inflation of historic proportions should have taught us that.

Mike Fox – head of Sustainable Investments at Royal London Asset Management

This said, it surprises us that many investors still talk with certainty about what 2023 will hold. In the best and more predictable of times, investment is a game of probabilities: there is no single future. These are not the most predictable of times, however, and we think it more beneficial to think about scenarios for this year rather than a singular outcome.

Investors often use the term ‘Goldilocks’ to describe the perfect financial conditions – neither too hot, nor too cold. This allows a decent level of growth without inflation at levels that would cause central banks concern. In today’s markets, this would be inflation coming back down to close to target levels of 2% without a significant recession, allowing interest rates to be reduced before the end of the year. In this scenario, most assets and investment styles would do well.

A modest recession would mean corporate profits remain robust, supporting equity investments generally, while the fall in interest rates would help growth investors. Bonds should also hold on to their recent gains and revert to playing their conventional role in portfolios.

Our first bearish scenario is centred on there being no historical precedent for inflation being brought under control without interest rates moving above the level of inflation, thereby creating positive real rates. Until this happens there is a risk that interest rate policy remains too accommodative. This implies that further rate increases are needed to bring down inflation, which would impact economic activity more negatively. Under this scenario, equity investing would be more challenging with defensive and more structural growth names probably outperforming. Bonds should hold their own, as rising rates and a recession more-or-less offset each other with respect to yields.

The second bear argument, perhaps paradoxically, involves economic growth this year being better than expected. Towards the end of 2022, the consensus view was that there would be a recession as much tighter monetary policy impacted areas such as employment and housing. Two events have challenged this view, however. First, the re-opening of China, which has happened much sooner and quicker than anyone expected. The world’s second largest economy has been constrained for three years, so consumers have significant money to spend on travel and all the things that we bought when we unlocked. After initial disruption as Covid spreads, this is likely to stimulate global growth and inflation.

The second event is the huge slice of luck that Europe has had with the weather. On Christmas Day it was 15°C in Berlin, something that has only happened twice before in history. This has removed the worst-case scenarios for energy shortages following the invasion of Ukraine. This has seen energy prices fall significantly – in some cases back to where they were before the invasion of Ukraine. Government support schemes will be significantly less expensive than expected, with businesses and consumers also benefiting.

In essence, the world’s second largest economy, China, and its largest economic region, Europe, are in much better shape than expected just a few months ago.

In this scenario, growth and inflation would surprise on the upside, which would create a dilemma for central banks. Do they raise interest rates further as inflation expectations increase again? Or do they accept more inflation? We would expect something of a repeat of last year, with rising interest and inflation expectations impacting both equity and debt markets, and energy/value outperforming.

Three scenarios and three different portfolio outcomes. It is hard to know which one will play out. ‘Goldilocks’ is clearly the most positive for asset owners, but the others require serious consideration. We observe the global economy being more resilient than expected, with higher employment and fewer catalysts for a global recession than a few months ago. This suggests growth and inflation may prove to be more resilient. However, we will only know in the fullness of time, so for now it is worth keeping an open mind.

Back in the real world

One of the defining characteristics of financial markets in the last year has been their almost-universal macro nature. It has mattered relatively little what a company does, simply whether it is ‘value’ or ‘growth’, and short duration or long duration. However, there is plenty going on at the company and industry level that we think will be positive for all investors, and sustainable investors in particular:

- Meaningful progress is being made in the treatment of cancer. A confluence of factors, including a greater understanding of the immune system and genetics, is allowing the next generation of cancer drugs to be developed and approved. We see AstraZeneca as a leading player in these developments.

- Renewable energy is being supercharged. In the short term, due to the war in Ukraine, more carbon-intensive forms of fuel, such as coal, are needed to ensure sufficient energy for all. However, far from creating a carbon renaissance, this is accelerating the rollout of renewable energy, both in the UK and abroad. Renewable energy is the energy of freedom and we believe that SSE will benefit.

- China is finally unlocking its population and country. After three years of Covid lockdowns, its citizens can now travel and consume as they did pre-pandemic. Given the lack of a government-backed health system and in the wake of the pandemic, many consumers are looking to purchase health and life insurance. Prudential could be a key beneficiary of this.

- The adoption of electric vehicles (EVs) is accelerating. Bloomberg estimates EV sales increased by 60% in 2022 and there are now 30m on the road compared to 10m at the end of 2020. In Norway, EVs are now four out of every five new cars sold. We believe that Texas Instruments benefits from this.

- The US Inflation Reduction Act that was passed in 2022 is an infrastructure investment programme to combat climate change, rebuild infrastructure and reduce dependence on foreign semiconductors. With $370bn of incentives and grants, this will be significant for both the US economy and those companies that provide relevant services to it. In our portfolios, Ferguson and Trane Technologies in particular could benefit from this.

(Please note: companies mentioned are held in at least one of our portfolios, but these are for illustrative purposes only and are not recommendations).

Balance is key

There are plenty of reasons to be optimistic, pessimistic or somewhere in between. There are risks, as ever, but also opportunities – and we will only know in time which are the most potent. In the meantime, having a balance of exposures across a range of industries that benefit from the observable trends is sensible. In addition, sustainability remains a key issue in business and society, and is an area worth focusing on. At some point, the outcome of the inflation / interest rates debate will be clear; once it is, the ‘real world’ of companies and their customers, rather than the purely macroeconomic one, will drive investment returns.

This is a financial promotion issued by Royal London Asset Management and is not investment advice. Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. Portfolio characteristics and holdings are subject to change without notice. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.

At Ethical Offshore Investments, we still have a high regard to the Sustainable Investing management skills of Mike Fox and his team at Royal London Asset Management. The Royal London Sustainable World Trust is held across our Sustainable Ethical Allocation model portfolios and the Sustainable Leaders Trust is also a recommended fund for exposure to UK sustainable and ethical companies.

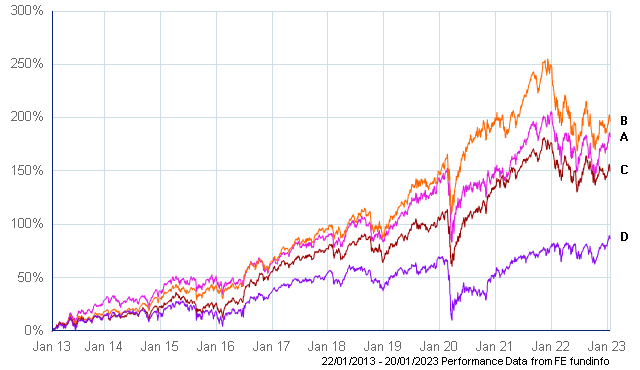

And the long term performance has rewarded investors…..

- Royal London Sustainable Leaders Trust C Acc (GTR 11.0%pa)

- Royal London Sustainable World Trust C Acc (GTR 11.5%pa)

- IA Global Index (GTR 9.7%pa)

- FTSE All Share Index (GTR 6.5%pa)

The above returns are net after management fees and dividends re-invested over the past 10 years.

Please note that this should not be regarded as individual investment advice and a recommendation to invest in the mentioned funds. Please speak to Ethical Offshore Investments (or your personal adviser) BEFORE you make any decision on investing in these funds to make sure that these managed funds are appropriate for your personal investment objectives.

Clients of Ethical Offshore Investments that invest into any of the Royal London Sustainable range of funds, will not incur any additional entry fee or buy/sell spread plus we will place the trade in the lowest charging version of the fund.

Sustainable Investing – Ethical Business Standards