Central banks were buying gold at record levels. Here’s why they’re selling now

Christoph Burgstedt /science Photo Library | Science Photo Library | Getty Images

The following news article was published by CNBC.

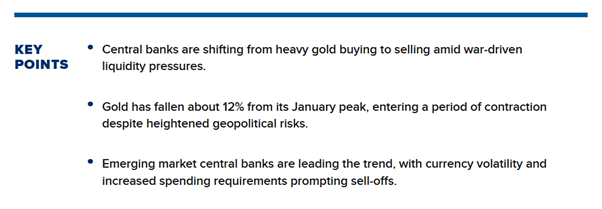

Gold’s pullback is exposing a rare shift in the market: after years of relentless accumulation, some central banks are now selling bullion as Iran war-driven pressures force a scramble for cash.

Spot gold, which is currently trading at around $4,838 per ounce, has fallen about 10% from its late-January peak, slipping into correction territory even as geopolitical risks intensify. The move marks a stark reversal from last year’s rally, when central bank buying helped underpin prices despite rising interest rates.

“There has been notable selling of gold by central banks from a few market participants,” Nicky Shiels, head of metals strategy at MKS Pamp, told CNBC.

The drivers are increasingly tied to wartime realities. Higher oil prices are straining import-dependent economies, while currency volatility is forcing some central banks to intervene more actively in foreign exchange markets, said market watchers.

Spending requirements are also a pressing consideration for central banks. “Many were sitting on a lucrative piggy bank with prices around $5,000 an ounce,” Shiels said. Some are now using gold reserves to “pay for increased energy and defense expenditure or to defend weakening currencies,” said Shiels.

Emerging market central banks appear to be at the forefront of this shift. A stronger U.S. dollar and higher borrowing costs are amplifying pressure on currencies, increasing the need for intervention.

“As far as gold is concerned, emerging market currency weakness has led some central banks to sell gold to stabilize currencies,” said Steve Brice, chief investment officer at Standard Chartered.

Concrete data on central bank sales tend to lag or remain discreet, but signs have been emerging.

Turkey has been the most notable seller so far this year. Its official gold holdings dropped by 131 tons in March through swaps and outright sales as authorities sought to stabilize the lira, according to a report published by Metals Focus last Thursday.

The Turkish lira has weakened further to breach new records since the Iran war began, falling about 1.7% against the U.S. dollar since conflict first broke out.

Similar patterns are visible elsewhere. Russia has reduced gold holdings in recent months, likely to help finance budget shortfalls, while Ghana has also sold reserves to boost foreign currency liquidity, data from Metals Focus showed.

Poland’s central bank governor also briefly explored selling part of its gold reserves to fund defense spending. The central European nation was the largest central bank buyer of gold in 2024 and 2025.

A strong demand pillar

The shift matters because central banks have been one of the strongest pillars of the gold market in recent years. Their steady buying helped offset outflows from Western investors and underpinned bullion’s surge to record highs. Now, both of those drivers appear to be reversing at the same time.

Central banks have been a dominant force in the gold market in recent years, buying more than 1,000 tons annually from 2022 — which marked the highest level of annual gold demand by central banks on record — through 2024, according to the World Gold Council. In 2025, central bank purchases declined to 863 tons as market participants navigated record-high price volatility.

“Our take behind the drop is that it is likely that some central banks are selling gold to defend their currency and/or to fund energy purchases,” Natixis said in a note, pointing to rising oil prices and a stronger U.S. dollar as key stressors.

While emerging markets appear to be driving recent sales, major reserve holders such as the Reserve Bank of India, People’s Bank of China and Bundesbank have remained largely opaque on their gold activity, underscoring the limited visibility into official sector flows.

The combination of retail investors exiting their gold positions and some central banks turning into net sellers has been among a key reason behind the recent drop, Natixis added.

Natixis also pointed to rising U.S. Treasury yields as another driver of outflows, with higher returns on fixed-income assets reducing the appeal of non-yielding bullion.

Similarly, Adrian Ash, director of research at BullionVault, said the logic is straightforward: gold bought as insurance ahead of a crisis can become a source of funding once that crisis hits.

“You bought gold in case of a crisis. Now crisis has struck,” he said.

“The rise in oil and gas, as well as the U.S. dollar and borrowing costs worldwide, will mean many central banks need to increase their FX reserves… and potentially defend their currency,” said Ash.

Still, industry veterans cautioned that these moves are often tactical rather than structural.

For one, the sales highlight gold’s role as a reserve asset in times of stress, said Shaokai Fan, global head of central banks at the World Gold Council.

“It really emphasizes why central banks hold gold… it’s a liquid asset that typically performs well during periods of uncertainty, and therefore they can deploy it if needed,” he told CNBC.

Additionally, major consumers like China have historically stepped in during price dips, and Natixis’ senior commodities analyst Bernard Dahdah said he expects opportunistic buying to re-emerge if prices fall further, potentially providing a floor.

How to get exposure to the Gold price movement

At Ethical Offshore Investments, our clients can get access to Gold (as well as other precious metals) through a range of different Exchange Traded Commodity (ETC’s) available on the various investment platforms. This is a very cost effective & secure way of holding physical Gold in your portfolio, without the need to worry about storage and insurance.

For example, the iShares Physical Gold ETC which is listed on the London Stock Exchange (as well as the Frankfurt, Italian and Mexican exchanges) holds the physical gold bars in secured and allocated storage in J.P. Morgan Chase, London branch vaults. The price movement of the ETC is based on the movement of the spot price of gold, less their management cost to cover storage and insurance of the Physical Gold, which is 0.12%pa.

We can also provide specialist investment products that can leverage on the gold price movement. If an investor is confident that the price of Gold will rise, we can offer a leveraged Exchange Traded Product on the spot price movement of Gold, where investors can get 2x up to 10x the price movement. Obviously this increases the risk as if the price goes down, it will also leverage the losses.

We can also provide specialist investment products that benefit from a falling asset price. So if an investor is confident that the price of Gold will fall, an investment in an ‘Inverse Gold ETC’ will provide a positive return if the Gold price was to fall. Same as above, this can also be leveraged to 2x – 10x the price movement to enhance returns (both positive and negative). Speak with Ethical Offshore to see how easy it is to get this type of exposure, with no additional entry and/or exit fees (apart from standard stock broker costs & stamp duty when applicable).

Please Note:

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy.

Please note the above article was first published by CNBC Business and should not be regarded as individual investment advice on whether to buy, sell or hold any of the investments mentioned. Please speak to Ethical Offshore Investors or your personal adviser BEFORE you make any investment decision based on the information contained within this article.

Lower costs resulting in more of the investment growth staying in your pocket.

Speak with Ethical Offshore Investments to learn how you can save on your investment costs.

Socially Responsible Investing – Ethical Business Standards